April 15, 2026

The GENIUS Act, Explained: What Enterprise Payment Teams Need to Know

*This article is for informational purposes only and does not constitute legal advice. The GENIUS Act and its implementing regulations are still evolving. Consult a qualified attorney before making compliance or business decisions based on this content

.png)

tl;dr

- The GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act), signed into law on July 18, 2025, created the first federal regulatory framework for USD-denominated stablecoins in the United States.

- For enterprise payment teams, the practical impact is straightforward: stablecoin payments in the US now have a clear legal basis, licensing structure, and compliance framework.

- The Act requires 100% reserve backing, monthly public disclosure of reserve composition, and gives stablecoin holders priority in bankruptcy. It’s designed to make stablecoins as regulated as any other payment instrument.

- The regulatory barrier that enterprise legal and compliance teams cited as the top reason to wait has been substantially removed.

Key Facts

- Full name: Guiding and Establishing National Innovation for U.S. Stablecoins Act

- Signed into law: July 18, 2025, by President Trump

- Senate vote: 68 to 30 (June 17, 2025)

- House vote: 308 to 122 (July 17, 2025)

- Effective date: January 18, 2027, or 120 days after final implementing regulations, whichever is earlier

- Reserve requirement: 100% backing with liquid assets (USD, short-term Treasuries)

- Disclosure: Monthly public reserve attestations required from all issuers

- Bankruptcy protection: Stablecoin holders have first-priority claims over all other creditors

The core obstacle to enterprise stablecoin adoption was not the technology. It was regulatory uncertainty — no federal licensing structure, unresolved jurisdictional questions, and fragmented state-level frameworks that made payment strategy difficult to plan around.

The GENIUS Act signed into law on July 18, 2025 resolves the core of that uncertainty.

This article is a practical guide to the GENIUS Act, what it means for enterprise payment operations.This is not legal advice (talk to your lawyers), but it is an overview of the framework that now governs payments stablecoin issuance in the United States.

But first…what is a stablecoin?

A stablecoin is a digital asset designed to maintain a stable value by being pegged to a reference asset, typically the US dollar. Unlike Bitcoin or other cryptocurrencies, which fluctuate in price, a USD-backed stablecoin is designed to always be redeemable at $1.

Stablecoins exist because moving money across borders through traditional rails is slow, expensive, and operationally cumbersome. A dollar-pegged stablecoin can move between counterparties in seconds, at a fraction of the cost of a wire transfer, with no banking hours or correspondent bank dependencies.

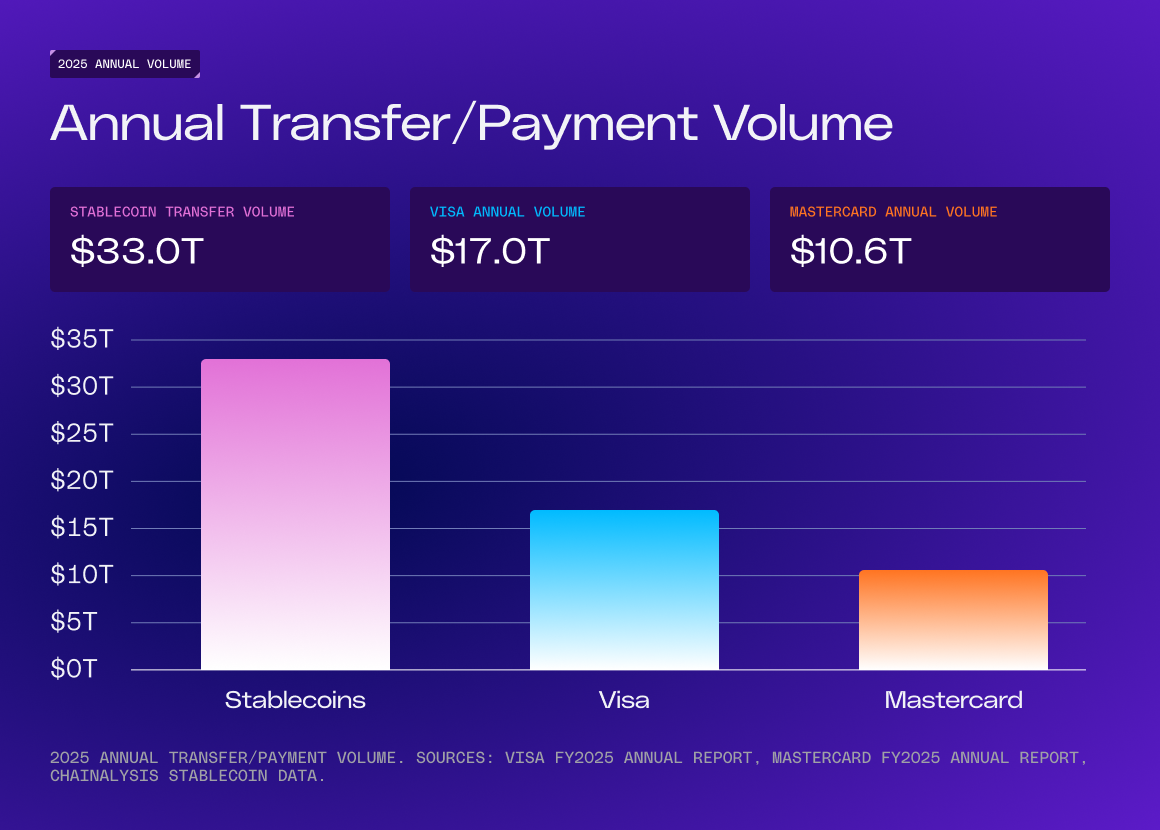

The market has grown substantially. Stablecoin market capitalization has grown at a compound annual rate of 77% over the past five years, reaching more than $250 billion. In 2025, stablecoin transfer volume reached $33 trillion, more than Visa and Mastercard combined. Enterprises from Stripe to BlackRock to Revolut are already operating on stablecoin rails in production.

What is the GENIUS Act?

The Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act) is the first comprehensive federal law governing digital assets in the United States. It passed the Senate 68 to 30 on June 17, 2025, and the House 308 to 122 on July 17, 2025, a notably bipartisan result. President Trump signed it into law the following day.

The law creates a federal licensing and supervisory framework specifically for "payment stablecoins," defined as digital assets that an issuer must redeem at a fixed monetary value. It does not cover crypto assets broadly, algorithmic stablecoins, or tokenized securities.

What does the GENIUS Act do?

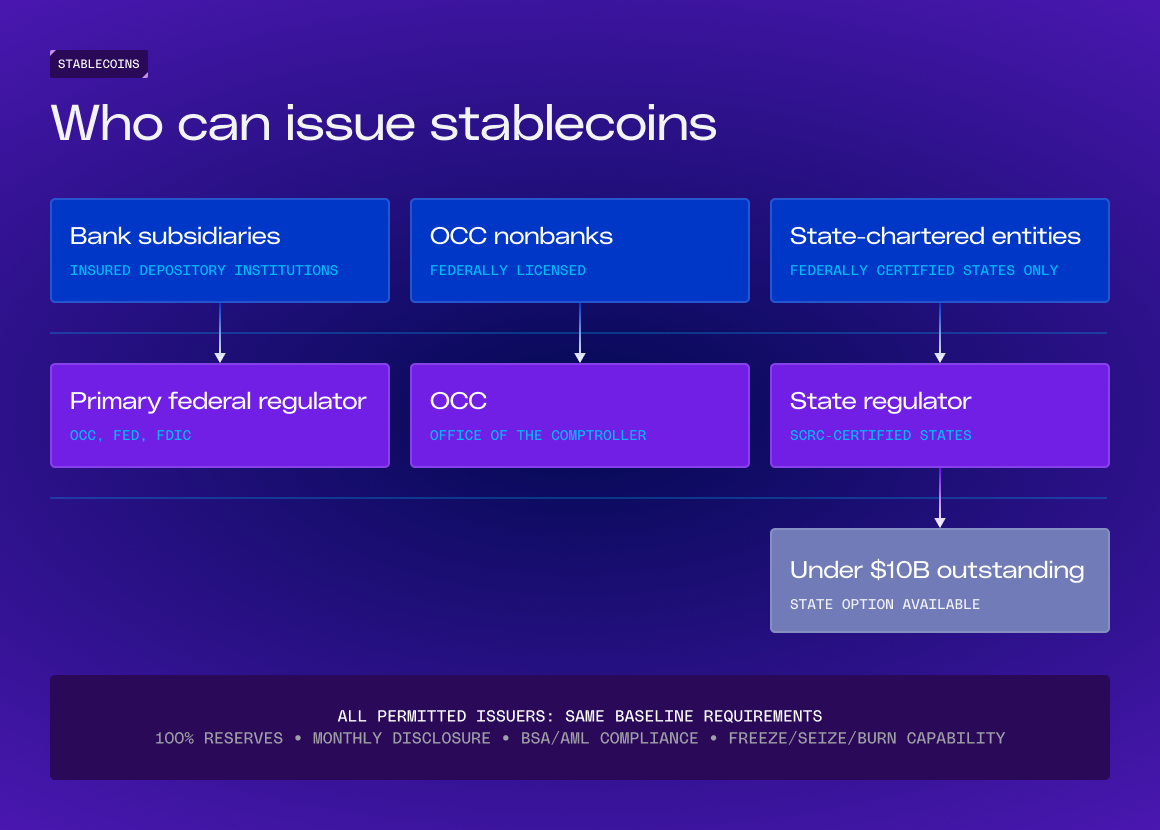

Who can issue stablecoins

Only three categories of entities may issue payment stablecoins in the US: subsidiaries of insured depository institutions (regulated by their primary federal banking agency), nonbank institutions supervised by the Office of the Comptroller of the Currency (OCC), and state-chartered entities operating under state regimes the federal government has certified as substantially equivalent to the federal framework.

Issuers with less than $10 billion in outstanding stablecoins may opt for state-level regulation under a qualifying state regime. Issuers above that threshold are subject to the full federal framework.

Reserve requirements

Permitted issuers must maintain reserves backing outstanding stablecoins on at least a 1 to 1 basis. Eligible reserve assets are limited to: US dollars and demand deposits at insured institutions, Treasury bills, notes, or bonds with maturities under 93 days, and repurchase agreements backed by Treasuries. Reserves cannot be rehypothecated except in limited circumstances. This is closer to money market fund regulation than to bank deposit regulation.

Disclosure and audit requirements

Issuers must publish monthly, public disclosures of reserve composition, certified by both the CEO and CFO, and examined by registered public accounting firms. Issuers with more than $50 billion in outstanding stablecoins are required to submit annual audited financial statements. This level of transparency exceeds what most traditional payment providers are required to disclose.

Consumer protection in bankruptcy

If a permitted issuer becomes insolvent, stablecoin holders have first-priority claims over all other creditors. Reserve assets are excluded from the debtor's estate. This is structural protection, not insurance, but it is meaningful. The law effectively ring-fences reserve assets for stablecoin holders.

Not a security, not a commodity

The Act explicitly excludes payment stablecoins issued by permitted issuers from the definitions of "security" under federal securities laws and "commodity" under the Commodity Exchange Act. This eliminates the SEC/CFTC jurisdictional uncertainty that stalled enterprise adoption for years. Stablecoins issued under the GENIUS Act are, unambiguously, payment instruments.

AML, KYC, and Bank Secrecy Act compliance

Permitted issuers are treated as financial institutions under the Bank Secrecy Act, which means they must maintain AML and sanctions compliance programs, including risk assessments, sanctions list verification, and customer identification. Enterprise compliance teams can evaluate GENIUS-compliant stablecoin providers using the same framework they use for any other payment infrastructure vendor.

Freeze, seize, and burn capability

All issuers must have the technical capability to freeze, seize, or burn payment stablecoins when required by a lawful order. This matters for enterprise counterparties that need to know stablecoin infrastructure can respond to legal process.

What the GENIUS Act does NOT do

Your legal team will ask about these. Be prepared.

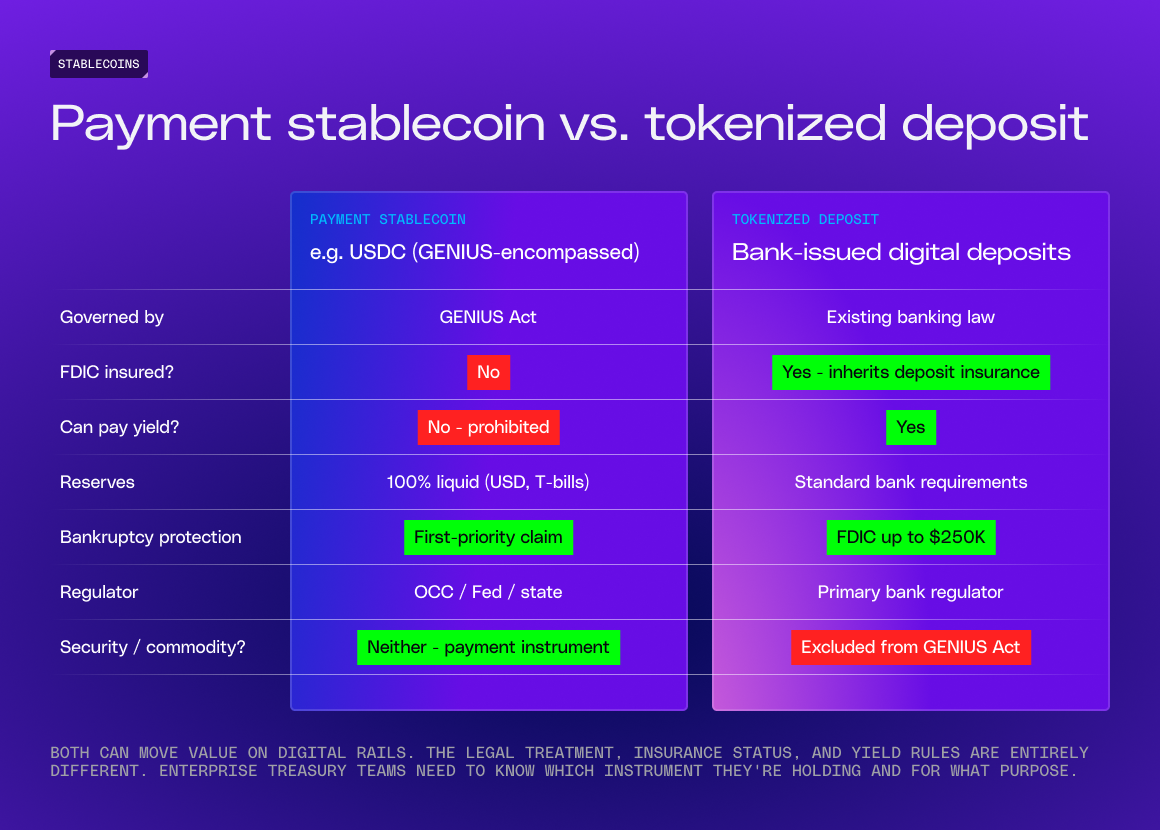

- It does not create FDIC insurance for stablecoin holdings. Stablecoins are not bank deposits. The bankruptcy priority provision provides structural protection, but it is different from deposit insurance.

- It does not permit yield or interest on payment stablecoins. Permitted issuers are explicitly prohibited from paying interest to stablecoin holders. This effectively bans yield-bearing stablecoins under the GENIUS framework. Enterprise treasury teams should not expect to earn returns on stablecoin balances held with a compliant issuer.

- It does not cover non-USD stablecoins. The framework is specific to USD-denominated payment stablecoins. Euro-denominated stablecoins fall under MiCA in the EU. Other currencies have their own frameworks.

- It does not cover tokenized deposits. Banks may continue to issue tokenized deposits, which are digital representations of bank deposits and retain FDIC insurance. Tokenized deposits can pay yield. They are legally distinct from payment stablecoins and are not covered by the GENIUS Act.

- It does not resolve all implementation details. The OCC, FDIC, and Federal Reserve are still issuing implementing regulations. Specific operational requirements, including application procedures, capital requirements, and examination standards, are being finalized through rulemaking.

What This Means for Enterprise Payment Operations

The GENIUS Act doesn’t change the mechanics of how stablecoins work. It changes the legal environment around them. For the enterprise payment ecosystem, the practical implications are:

Legal basis for adoption: permitted stablecoin issuers now have a federal framework to evaluate, rather than navigating a patchwork of state money transmitter laws and SEC/CFTC jurisdictional uncertainty. The framework is clear: stablecoins are payment instruments, regulated as such.

Provider evaluation criteria: The GENIUS Act gives enterprise payments teams specific requirements to ask stablecoin infrastructure providers. Are they working with a permitted payment stablecoin issuer? What’s the reserve composition? Is the issuer publishing monthly disclosures? Are they subject to federal or state supervision? These questions now have definitive regulatory answers.

Compliance integration: The Act subjects permitted issuers to the Bank Secrecy Act, meaning they must maintain AML and sanctions compliance programs with risk assessments, sanctions list verification, and customer identification. Enterprise compliance teams can evaluate stablecoin providers using the same framework they use for any other payment infrastructure vendor.

Timeline: The GENIUS Act takes effect on the earlier of 18 months after enactment (January 2027) or 120 days after final implementing regulations are issued. During this transition period, existing stablecoin operations continue under current state-level frameworks.

What does the GENIUS Act mean for cross-border operations?

Enterprises operating across multiple jurisdictions need to understand one additional provision. The GENIUS Act prohibits digital asset service providers from offering or selling stablecoins issued by a foreign issuer to US customers, unless that foreign issuer comes from a jurisdiction the US Treasury Secretary has certified as having a comparable regulatory framework, and can demonstrate the ability to comply with US lawful orders, including regulatory asset freezes and sanctions compliance.

Foreign issuers that meet these conditions must register with the OCC and hold reserves in a US financial institution sufficient to meet liquidity demands of US customers. The practical effect is that enterprise treasury and payments teams should verify, for any stablecoin infrastructure they use across jurisdictions, that the issuer either qualifies under the GENIUS Act or operates under a jurisdiction the Treasury Secretary has approved.

For the broader regulatory picture: the EU's MiCA regulation governs euro-denominated stablecoins. Hong Kong, Singapore, and Japan each have operating stablecoin licensing frameworks. The regulatory landscape has shifted from "unclear in most markets" to "regulated in most major financial markets." The remaining gaps are primarily in developing economies, which are often the corridors where stablecoin payments offer the greatest cost advantage.

What is the CLARITY Act, and how does it relate?

The US House passed the Digital Asset Market Clarity Act of 2025 (CLARITY Act), which provides a broader regulatory structure for non-stablecoin digital assets and clarifies the oversight roles of the SEC and CFTC. The two laws are designed to be complementary. GENIUS handles payment stablecoins as payment instruments. CLARITY would handle the rest of the digital asset market structure question. Clarity Act has not been signed into law yet.

The Global Regulatory Picture

The GENIUS Act doesn’t exist in isolation. The EU’s Markets in Crypto-Assets (MiCA) regulation is fully applicable, providing a comparable framework for euro-denominated stablecoins. Hong Kong enacted its Stablecoin Bill. Singapore has a licensing framework. Japan has authorized yen-denominated stablecoins under its Payment Services Act.

For enterprises operating across multiple jurisdictions, the regulatory picture has shifted from “unclear in most markets” to “regulated in most major financial markets.” The remaining gaps are primarily in developing economies, which are typically the corridors where stablecoin payments offer the greatest cost advantage.

GENIUS Act Provider Evaluation Checklist

- Is the stablecoin issuer a permitted payment stablecoin issuer under the GENIUS Act?

- Is the issuer supervised by the OCC (for nonbanks), a primary federal banking regulator (for bank subsidiaries)?

- Does the issuer publish monthly public disclosures of reserve composition, certified by senior executives and examined by a registered public accounting firm?

- Is the reserve backed 100% by eligible liquid assets (USD, short-term Treasuries, repos backed by Treasuries)?

- Does the issuer maintain AML, KYC, and sanctions compliance programs meeting Bank Secrecy Act requirements?

- Does the issuer have the technical capability to freeze, seize, or burn stablecoins in response to lawful orders?

- If the issuer is foreign: has the US Treasury certified the issuer's home jurisdiction as having a comparable framework? Has the issuer registered with the OCC and hold US-based reserves?

- Does the issuer explicitly prohibit yield or interest payments on stablecoin holdings (confirming compliance with the non-interest prohibition)?

What to Do Next

If your organization has been waiting for regulatory clarity, the wait is substantially over. The practical next step is to brief your legal and compliance teams on the GENIUS Act framework, evaluate whether your current stablecoin infrastructure providers (or potential providers) meet the permitted issuer criteria, and begin scoping a pilot in a specific corridor.

Polygon’s network has processed $2.4 trillion in stablecoin transfer volume, with partners including Mastercard, Revolut, Stripe, and BlackRock operating in production under existing regulatory frameworks. The GENIUS Act provides the federal foundation for the next wave of enterprise adoption.

Evaluate Stablecoin Infrastructure Under the New Framework

Learn more at polygon.technology, or talk to our team about how the GENIUS Act framework applies to your payment operations.

*NOTE: Polygon Labs is not a stablecoin issuer and does not issue, redeem, or control any stablecoin.

What is a payment stablecoin under the GENIUS Act?

The GENIUS Act defines a payment stablecoin as a digital asset that is issued for use as a means of payment or settlement, and that the issuer is obligated to redeem at a fixed amount of monetary value. The definition explicitly excludes national currencies, bank deposits (including tokenized deposits), and securities. Tokenized money market funds, for example, are still regulated as funds, not as payment stablecoins.

What is the difference between a payment stablecoin and a tokenized deposit?

A tokenized deposit is a digital representation of a bank deposit. Tokenized deposits retain FDIC insurance, can pay yield or interest, and are explicitly excluded from the GENIUS Act's definition of a payment stablecoin. Banks may continue to issue tokenized deposits under existing banking authority. Payment stablecoins, by contrast, are not FDIC-insured, cannot pay interest under the GENIUS Act, and are subject to the GENIUS Act's reserve, disclosure, and supervisory requirements. For enterprise treasury teams, this is a meaningful distinction when evaluating which instrument to hold and for what purpose.

Does the GENIUS Act cover stablecoin operations outside the US?

The GENIUS Act governs payment stablecoins issued by permitted US issuers and establishes conditions under which foreign-issued stablecoins may be offered to US customers. For cross-border operations, enterprises should verify that their stablecoin infrastructure providers are compliant under the jurisdictions in which they operate. The EU's MiCA regulation governs euro-denominated stablecoins. Singapore, Hong Kong, and Japan each have operating stablecoin frameworks. Most major financial markets now have regulatory structures in place.

What should enterprise payments teams evaluate about stablecoin providers under the GENIUS Act?

Whether the provider's stablecoin issuer is a permitted payment stablecoin issuer under the Act. The composition and public disclosure schedule of reserves. Whether the issuer is subject to federal or state supervision under the GENIUS framework. Whether compliance programs (KYC, AML, sanctions screening) meet Bank Secrecy Act requirements. Whether the issuer publishes monthly reserve attestations certified by senior executives and examined by a public accounting firm. And, for foreign issuers: whether the issuer's home jurisdiction has been certified by the US Treasury Secretary as having a comparable framework, and whether the issuer has registered with the OCC.

.png)