tl;dr

- Cross-border B2B payments cost businesses an estimated $120 billion in transaction fees every year

- The real damage isn’t from the wire fee, but an FX markup and charges deducted mid-transit, alongside the lockup of working capital between time zones

- Traditional cross-border payments are orders of magnitude more expensive than an onchain transaction

- Modern payment infrastructure can reduce these costs by 90%+ while settling in seconds, not days or hours

A 0.1% transaction fee sounds like nothing.

On a $500,000 payment, that’s $500. A rounding error on a deal that size.

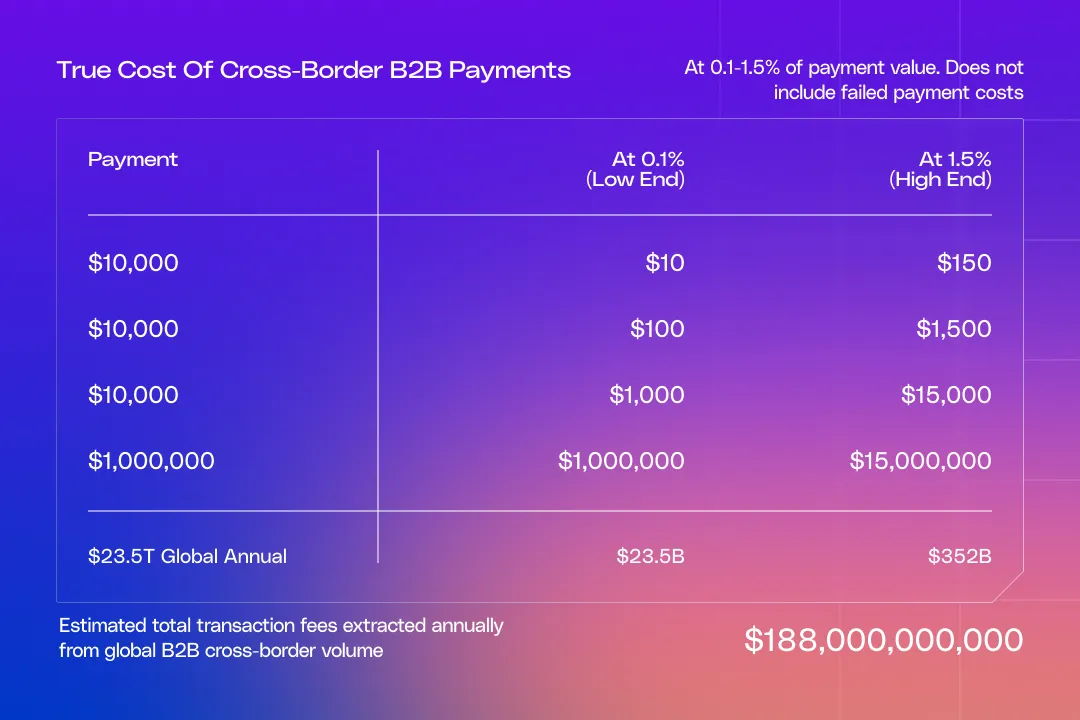

Now ramp it up to $145 trillion, the annual volume of wholesale B2B payments crossing borders. That 0.1% becomes $145 billion. Per year. For retail B2B, the rate is even higher–1.5%.

It doesn’t have to be like this.

Onchain settlement runs a fraction of a cent per transaction, making each 0.1% or 1.5% transaction seem enormous when there are enormous payments flow. There’s no lockup for onchain transactions. Instead, instant settlement, at internet speed.

The infrastructure to move money at near-zero cost and near-zero wait time is already in production.

Most businesses just aren’t using it yet.

What it actually costs to send cross-border transactions

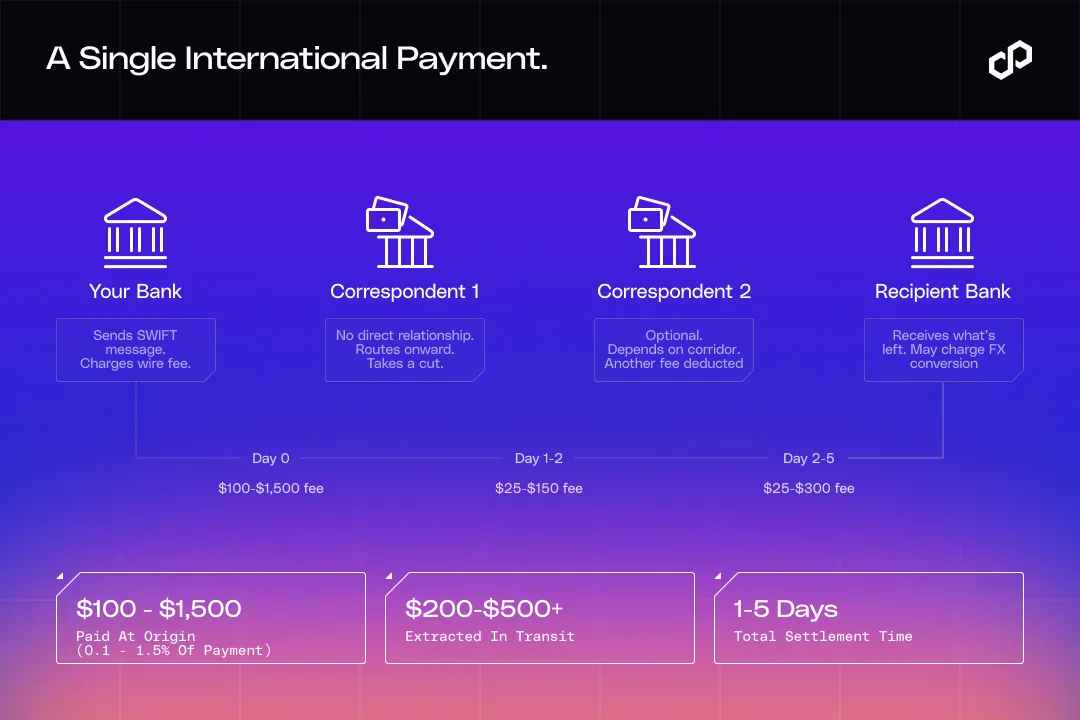

A cross-border B2B payment touches more hands than most people realize. Here’s the anatomy of a single international wire:

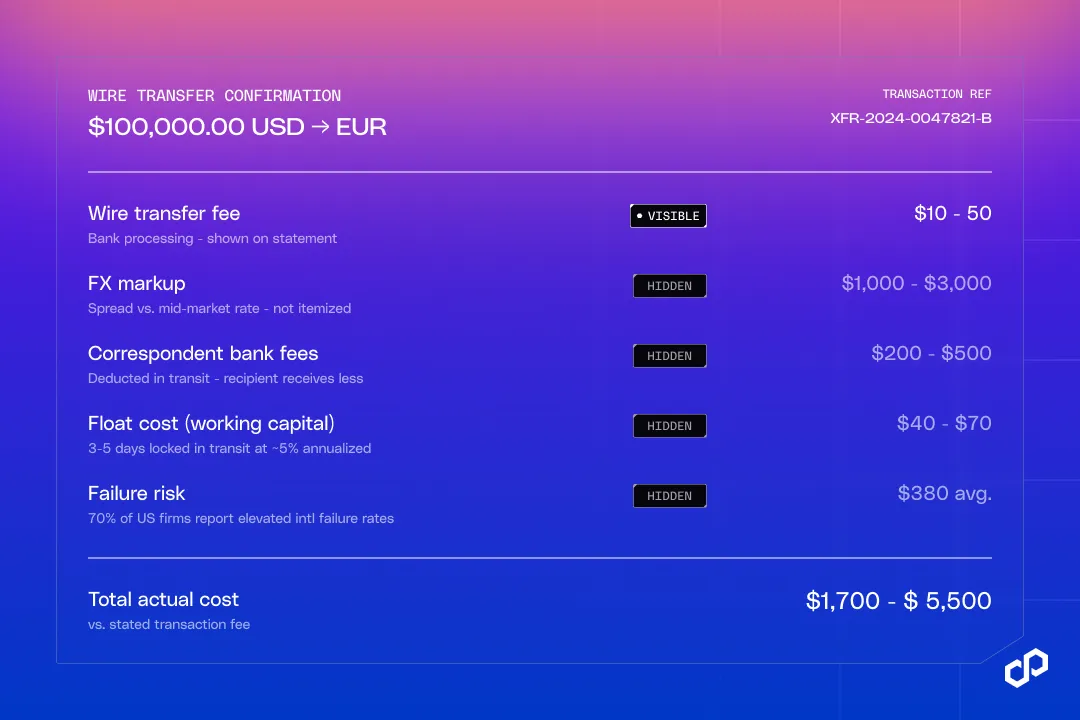

The wire fee is the only cost most people see. Banks charge $15–$50 per SWIFT transaction, depending on the corridor and your relationship. It’s real, but it’s the smallest line item in the actual cost structure.

The FX markup make things more expensive. When banks convert currencies, they add a spread, which varies from bank to bank, corridor to corridor, and type of transaction. What it means is: the fee is baked into the rate, and you’d need to compare against the interbank rate in real time to see it.

Correspondent bank charges are another wild card. SWIFT doesn’t actually move money, it sends messages between banks. If your bank and the recipient’s bank don’t have a direct relationship (and they often don’t), the payment routes through one, two, sometimes three intermediary banks. Each takes a small cut. These fees are often deducted directly from the payment amount in transit, meaning the recipient often gets less than you sent.

Float and working capital cost is the silent killer. Even the fast SWIFT gpi payments can take a full day to settle; other cross-border transactions may take longer. During that window, your money exists in a kind of limbo. Industry estimates put nearly $12 billion in working capital floating in transit across SWIFT at any given moment. For any business operating on tight margins or managing cash flow across multiple currencies, that’s capital you can’t deploy, earning nothing.

Failed payment costs complete the picture. Cross-border payments fail at significantly higher rates than domestic ones. 70% of U.S. firms report higher failure rates on international transfers. When a payment fails, it doesn’t just bounce back instantly. It reverses through the same chain of intermediaries, often with fees deducted at each step. Failed cross-border payments cost U.S. merchants an estimated $3.8 billion per year in lost sales alone.

Add It Up

The headline numbers look lean. Wholesale B2B payments cost around 0.1% on average. Retail B2B runs about 1.5%. Compared to the 6% fees on remittances, these seem almost negligible.

But lean percentages on massive volumes add up to enormous losses, over time. A multinational paying a $50 million invoice to a foreign supplier loses $50,000 to that 0.1% wholesale fee. A mid-sized manufacturer wiring $500,000 to an overseas parts vendor pays $7,500 at the 1.5% retail B2B rate. Every month, that’s $90,000 a year on a single supplier relationship.

And those percentages don’t capture the full picture: trapped liquidity while payments clear, operational overhead from reconciliation across time zones, and the downstream cost when payments fail or arrive short.

This is a story about infrastructure that hasn’t kept pace with what’s now possible.

The Opportunity in Front of Us

The correspondent banking model that underpins SWIFT was built in the 1970s. It has been upgraded since, with SWIFT gpi, launched in 2017, bringing tracking, speed, and fee transparency to cross-border payments. Today, nearly 60% of gpi payments credit within 30 minutes, and almost all settle within 24 hours. That’s real progress.

But gpi is an optimization layer on top of the original architecture, not a digital upgrade. The fundamental structure that involves multiple intermediaries, sequential processing, nostro/vostro account funding, and more fees remains intact. Each node still needs to be compensated. Each handoff still introduces latency. Capital still gets trapped

The G20 recognized the limits of incremental improvement in 2020, setting targets to bring cross-border payment costs below 1% for retail and 3% for remittances by 2027. A December 2025 BIS report acknowledged those targets are unlikely to be met on time. The global average cost of sending remittances actually ticked up in early 2025, to 6.49%.

The industry has been working on this for years, making genuine headway. But there’s a ceiling to what you can achieve by optimizing legacy rails.

At some point, the opportunity shifts from better plumbing to better infrastructure, giving institutions that move money fundamentally better tools.

What Modern Infrastructure Looks Like

Stablecoin payment rails settle in seconds, not business days. The total transaction cost is a fraction of a percent. This represents transactions that are orders of magnitude less expensive, even with FX rates. There are no correspondent banks in the chain, no hours- or days-long float eating your working capital.

Polygon has processed over $2.4 trillion in stablecoin transfer volume. It’s throughput at scale, running continuously, with the kind of uptime that enterprise payments demand. The infrastructure handles the settlement. The business gets the speed, the cost savings, and the transparency that the legacy system structurally cannot provide.

Move money at the speed and cost it deserves. Learn how the Open Money Stack is replacing legacy payment rails for enterprises worldwide, or talk to our team about what modern payment infrastructure looks like for your business. Polygon’s payments infrastructure is built for exactly this — see how it works.

Custodial vs. Non-Custodial Wallets: Which One Should Your Platform Build?

Move Money Between Solana and Polygon, Ethereum, Base + more EVM Chains with Polygon OMS

.CXtdIGFA_Z2ODqj.webp)

Ithaca Upgrade Is Live: Payments on Polygon Chain Are More Reliable Than Ever

Kansai Electric Power's Rewards Arm Turns Loyalty Points Into Real Stablecoin Payments on Polygon Chain

Mento Protocol Launches on Polygon for Local Currency Stablecoin Payments

PayPal USD Lands on Polygon Chain, Enabling Regulated Onchain Dollars to Move Across Borders in One Integration

Credible Races Past $152M Total Payments Volume on Polygon

We Built the Best Blockchain for Payments. Now We’re Bringing the World’s Enterprises Onchain

Uquid Integrates Polygon's Open Money Stack for 1-Click Crypto Checkout Across 178M+ Products

.Cfn0LZ0R_2iwkGz.webp)