tl;dr

- A stablecoin sandwich is a cross-border payment method that wraps a stablecoin transfer between two fiat currency conversions: local currency in, stablecoin across, local currency out.

- It’s the dominant pattern for enterprise stablecoin payments today. Stripe, Visa, Mastercard, and most B2B payment platforms building on stablecoin rails use this architecture.

- The settlement leg (the stablecoin transfer in the middle) takes seconds. The fiat conversion at each end is where the remaining friction lives, and that friction is shrinking as on-ramp and off-ramp infrastructure matures.

If you’ve been researching how enterprise stablecoin payments actually work, you’ve probably encountered the term “stablecoin sandwich.” It’s shorthand for the payment architecture that has become the de facto standard for cross-border stablecoin settlement.

This article explains what a stablecoin sandwich is, how it works mechanically, why it emerged as the dominant pattern, and what to look for when evaluating infrastructure that supports it.

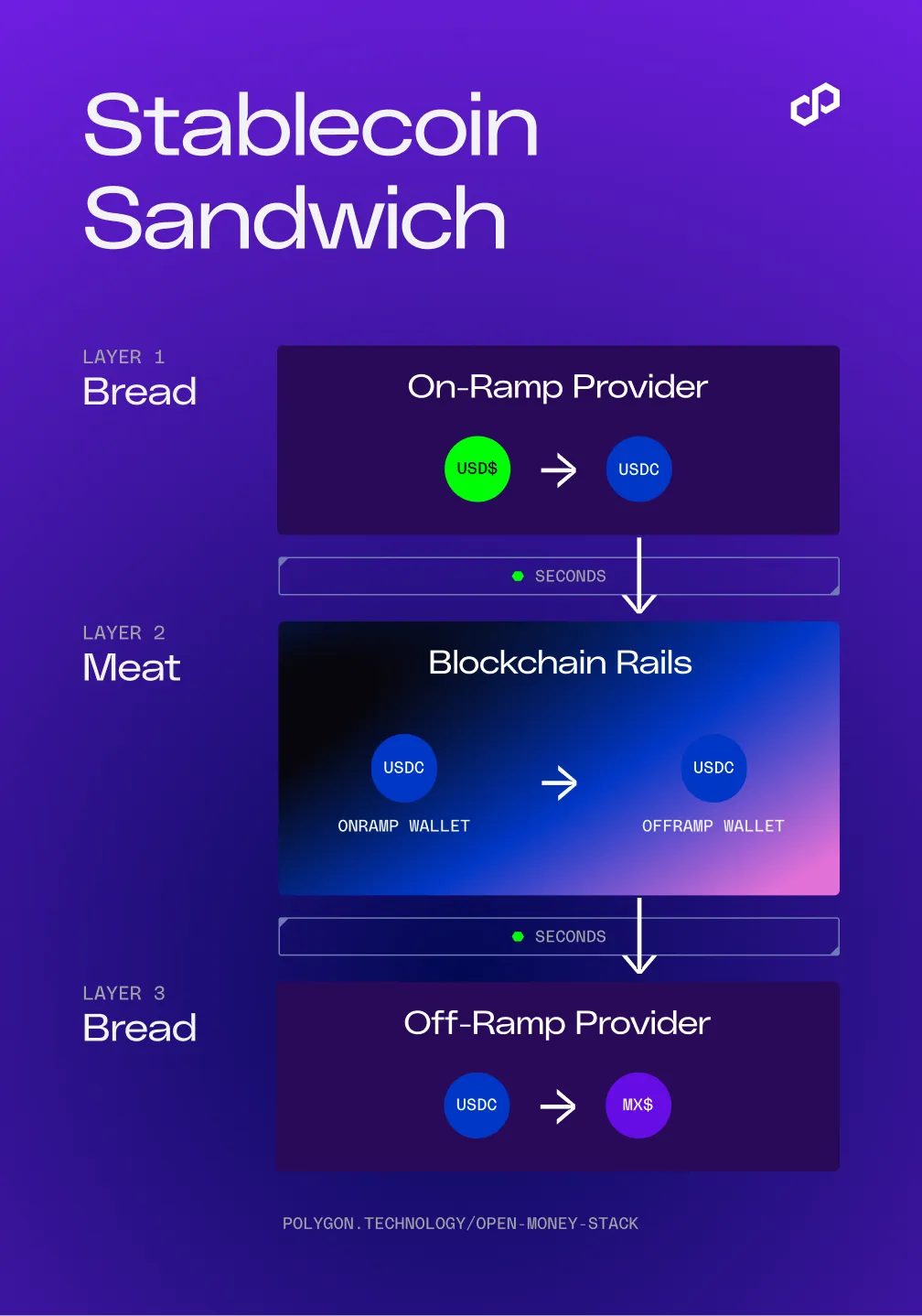

The Three Layers

A stablecoin sandwich has three distinct steps:

1st, a piece of bread: Fiat on-ramp

The sender’s local currency (USD, EUR, GBP, BRL, or any other fiat currency) is converted into a stablecoin, typically USDC or USDT. This conversion happens through a licensed money services business or payment provider that handles KYC/KYB, compliance screening, and the actual currency exchange.

2nd, meat: Stablecoin transfer

The stablecoin moves across the settlement network from the sender’s side to the receiver’s side. This is the fast part. On a network like Polygon, this transfer settles in seconds, costs approximately $0.002, and operates 24/7/365. There are no intermediary banks, no correspondent chains, no banking hour restrictions.

3rd, another piece of bread: Fiat off-ramp

The stablecoin is converted back into the recipient’s local currency and delivered to their bank account. This step also requires a licensed provider in the recipient’s jurisdiction, handling KYC/KYB, AML screening, and local currency delivery.

The sandwich metaphor is implicit in the structure: fiat bread on both sides, stablecoin filling in the middle. The sender deals in fiat. The recipient receives fiat. The stablecoin layer in between is the infrastructure.

A Real-world Example: USD to MXN

Abstract mechanics are easier to follow with a concrete example. Here’s what a stablecoin sandwich looks like for a US company paying a supplier in Mexico.

The scenario. A US-based manufacturer needs to pay a Mexican parts supplier $50,000 USD.

The stablecoin sandwich route goes:

1. The manufacturer’s payment platform converts $50,000 USD to USDC through its licensed on-ramp provider. Compliance screening (KYC/KYB, AML) happens here. This step takes seconds to minutes.

2. The USDC transfers across the settlement network to the Mexican off-ramp provider’s address. This step takes seconds. Cost: less than $0.01.

3. The Mexican off-ramp provider converts the USDC to pesos at the prevailing market rate and deposits into the supplier’s bank account. This step completes same-day, often within hours.

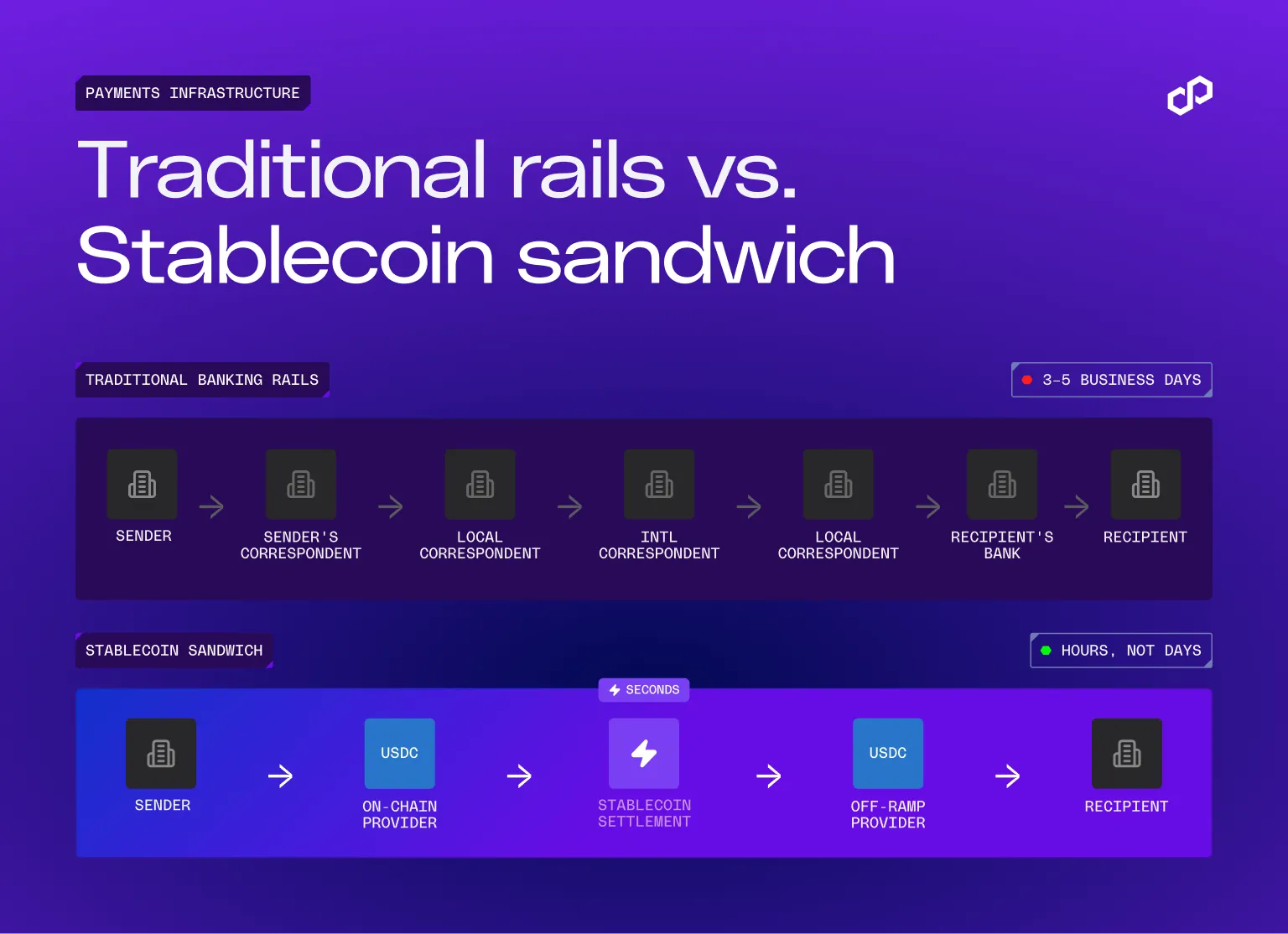

Total elapsed time: minutes to hours, not hours to days.

Total cost: well below what correspondent banking charges for this corridor.

Why This Pattern Emerged

The stablecoin sandwich solves a specific problem: how do you get the speed and cost advantages of stablecoin settlement without requiring senders or recipients to hold, manage, or even think about stablecoins?

Most enterprises don’t want to hold stablecoins on their balance sheet. Their treasury teams work in fiat. Their accounting systems report in fiat. Their suppliers invoice in fiat. Asking an enterprise to adopt stablecoins as a treasury instrument is a much bigger lift than asking them to route payments through stablecoin rails.

The sandwich pattern makes stablecoin settlement invisible to the end users on both sides. The sender sends dollars (or euros, or pounds). The recipient receives their local currency. The fact that the payment traveled as USDC across a settlement network for a few seconds in between is an infrastructure detail, not a user-facing change.

This is exactly the architecture that Stripe, Visa, Mastercard, and most serious B2B platforms are building around. The user interface stays in fiat. The settlement infrastructure underneath uses stablecoins.

Where the Speed Actually Lives (and Where the Friction Remains)

The settlement leg of the sandwich (the meat) is genuinely fast. On Polygon, a stablecoin transfer settles in seconds. This part of the process has been solved at scale, with over $2.4+ trillion in stablecoin transfer volume processed on the network.

The friction in the stablecoin sandwich lives at the edges: the on-ramp and off-ramp. Converting fiat to stablecoins and back requires licensed providers in each jurisdiction, KYC/KYB verification, AML screening, and integration with local banking rails. The speed of these steps depends on the provider, the corridor, and the regulatory environment.

In optimized setups with integrated on-ramp and off-ramp providers, end-to-end fiat-to-fiat settlement takes hours rather than days. Some corridors achieve same-hour delivery. That’s not instant, but compared to 1 to 5 business days through correspondent banking, it represents a step change.

The maturation of on-ramp and off-ramp infrastructure is the single biggest factor determining how fast the stablecoin sandwich gets for enterprise users. As licensing coverage expands and ramp providers integrate more deeply with local payment systems, the edges of the sandwich will get faster. The middle is already solved.

Full Sandwich vs. Open Sandwich

There are two meaningful variations worth understanding.

Full stablecoin sandwich. The end-to-end automated flow: fiat in, stablecoin across, fiat out. Neither the sender nor the recipient interacts with stablecoins at any point. Conversion is handled automatically by on-ramp and off-ramp providers. This is the standard architecture for B2B payment platforms, payroll, and vendor payouts.

Open (or half) stablecoin sandwich. In this variation, the recipient receives stablecoins rather than converting back to fiat immediately. The sender still converts fiat to stablecoins on their end. But the recipient, whether a treasury team with multicurrency exposure, a platform managing float, or a business in a high-inflation market, chooses to hold the stablecoin temporarily. The fiat off-ramp happens later, or not at all.

The open sandwich is less common in pure B2B payment flows but relevant for platforms managing liquidity, digital-native businesses, and businesses operating in environments where holding USD-pegged stablecoins is preferable to holding local currency.

Risks and Regulatory Considerations

The stablecoin sandwich offers real speed and cost advantages, but it comes with operational and compliance considerations that any enterprise should understand before deploying at scale.

Regulatory jurisdiction coverage

On-ramp and off-ramp providers must hold the relevant money transmission licenses in every jurisdiction where payments originate or land. In the US, the benchmark is 48-state coverage. Internationally, coverage varies significantly by corridor. A provider with strong EU coverage may have limited reach into Southeast Asia or sub-Saharan Africa. Verify licensing specifically for the corridors that matter to your payment flows, not just the corridors the provider highlights in its marketing.

AML and KYC architecture

Compliance requirements don’t disappear in a stablecoin sandwich. They shift. KYC/KYB and AML screening happen at the on-ramp and off-ramp layers. The key question is whether compliance is built into the API or requires separate tooling. Providers with compliance built into the integration, such as the Polygon Open Money Stack, are significantly easier to operate at scale. Compliance as an afterthought will slow payments and create operational overhead. bolted

Settlement layer reliability

Not all stablecoin settlement networks are equivalent. Production volume under real conditions is different from sandbox performance. For enterprise payment flows where downtime means broken supplier relationships and delayed payroll, uptime track record and production volume matter as much as technical specifications.

Regulatory trajectory

The regulatory environment for stablecoin payments has been moving in a favorable direction. In the US, the GENIUS Act represents the first comprehensive federal framework for stablecoin issuance and payment. In the EU, MiCA (Markets in Crypto-Assets regulation) established a licensing regime for stablecoin issuers and service providers that came into full effect in 2024. These frameworks create clearer compliance pathways for enterprise adoption. The direction of travel is toward greater regulatory clarity.

FX risk at the edges

The stablecoin transfer in the middle of a sandwich is stable by design. USDC and USDT maintain their peg. But the fiat conversion steps on each end involve real exchange rates. The spread and timing of those conversions determine your total FX cost. For high-volume corridors, this is worth negotiating explicitly with your on-ramp and off-ramp providers.

What to Evaluate in a Stablecoin Sandwich Provider

Not all stablecoin sandwich implementations are equal. The quality of the experience depends on how well the three layers are integrated. Key criteria:

- On-ramp licensing coverage

The provider needs money transmission or equivalent licenses in the jurisdictions where your payments originate. For US operations, 48-state coverage is the benchmark. Gaps in licensing mean gaps in your payment corridors.

- Off-ramp coverage and speed

The provider needs licensed off-ramp partners in your destination markets. Ask specifically about delivery times for your key corridors. “Same-day settlement” in the provider’s best corridor may not reflect reality in your actual payment mix.

- Settlement layer reliability

The network processing the stablecoin transfer needs proven volume at scale, not sandbox performance. A network that has processed trillions is a different category of proven than one that has processed a few million on testnet.

- Single integration vs. multiple contracts

The cleanest implementations let you access all three layers (on-ramp, settlement, off-ramp) through a single API integration. Every additional provider contract is an additional point of friction, failure, and negotiation.

- Compliance architecture

KYC/KYB and AML screening happen at the on-ramp and off-ramp layers. Ask whether compliance is built into the API or requires separate tooling. Compliance bolted on as an afterthought will slow down your payments and create operational overhead.

How Polygon Fits In

The Polygon Open Money Stack is being built to bring all three layers together: fiat on-ramps (operation in 48 US states through Coinme via money-transmitter licenses and compliance infrastructure), the settlement layer, and wallet infrastructure, accessible through a single API. The goal is to make the full stablecoin sandwich available through one integration point, rather than requiring enterprises to stitch together on-ramp, settlement, and off-ramp providers separately.

The Polygon chain is the settlement layer (Layer 2) in the stablecoin sandwich for many of the largest enterprise payment flows running on stablecoin rails today. Over $2+ trillion in stablecoin transfer volume has settled on the network, with partners including Mastercard, Revolut, Stripe, and Paxos.

Learn More About Stablecoin Payment Infrastructure

Learn more at polygon.technology, or talk to our team about how the stablecoin sandwich architecture works for enterprise payment flows through the Polygon Open Money Stack.

Custodial vs. Non-Custodial Wallets: Which One Should Your Platform Build?

Move Money Between Solana and Polygon, Ethereum, Base + more EVM Chains with Polygon OMS

.CXtdIGFA_Z2ODqj.webp)

Ithaca Upgrade Is Live: Payments on Polygon Chain Are More Reliable Than Ever

Kansai Electric Power's Rewards Arm Turns Loyalty Points Into Real Stablecoin Payments on Polygon Chain

Mento Protocol Launches on Polygon for Local Currency Stablecoin Payments

PayPal USD Lands on Polygon Chain, Enabling Regulated Onchain Dollars to Move Across Borders in One Integration

Credible Races Past $152M Total Payments Volume on Polygon

We Built the Best Blockchain for Payments. Now We’re Bringing the World’s Enterprises Onchain

Uquid Integrates Polygon's Open Money Stack for 1-Click Crypto Checkout Across 178M+ Products

.Cfn0LZ0R_2iwkGz.webp)