tl;dr

- The Open Money Stack is being built as one API for the full payment journey, not a collection of best-of-breed endpoints

- This is in contrast to enterprise payment stacks today, which involve 5 to 8 APIs from different vendors, each with its own data model, error handling, and lifecycle

- More APIs create more surface area for failure, more reconciliation overhead, and more engineering maintenance that has nothing to do with your core product

- The payment industry’s focus on API-first design has produced better individual components and worse overall systems

Ask any payment infrastructure vendor about integration and you’ll hear the same pitch: “We have a well-documented API. Integration takes days, not months. Here’s the sandbox.”

It’s often true. Individual APIs are better designed than ever. Documentation is cleaner, SDKs exist for every major language, sandbox environments are functional.

Each individual piece is genuinely good.

So why do enterprises find payment infrastructure still so painful to manage?

Because the problem was never any single API. The problem is that you need seven of them, and nobody designed them to work together.

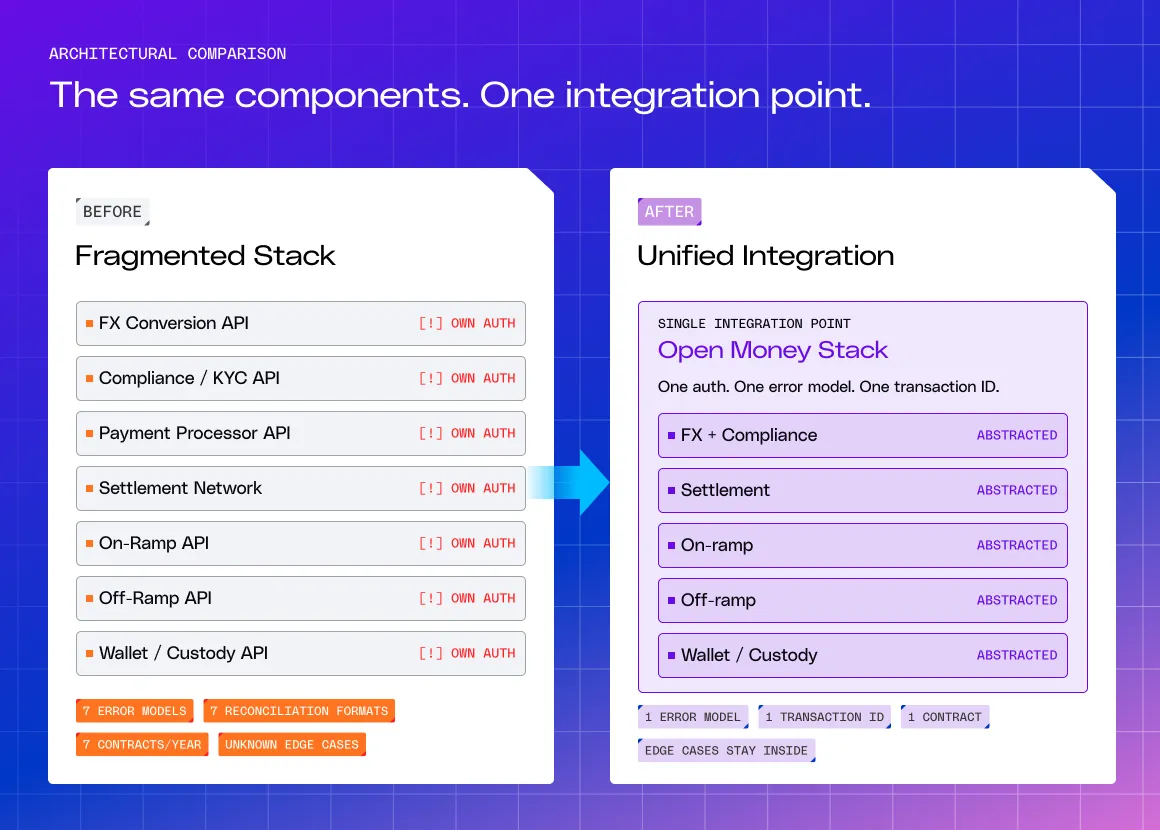

The Anatomy of an Enterprise Payment Stack

Here’s what a modern cross-border enterprise payment stack actually looks like:

FX conversion API: Handles currency exchange. Has its own rate feed, its own markup model, its own error codes for when a rate expires mid-transaction.

Compliance/screening API: Handles KYC/KYB verification and sanctions screening. Has its own onboarding flow, its own response format for flagged transactions, its own webhook structure for status updates.

Payment processor API: Initiates and tracks payment instructions. Has its own transaction ID system, its own status taxonomy (“pending,” “processing,” “settled” might mean different things depending on the provider).

Settlement network: Moves the value. Has its own confirmation model, its own finality definitions, its own timing guarantees.

On-ramp API (if using stablecoin rails): Converts fiat to stablecoins. Has its own KYC flow (possibly duplicating the compliance API), its own rate quotes, its own settlement timing.

Off-ramp API: Converts stablecoins back to fiat at the destination. Same duplication: its own KYC, rates, timing, error handling.

Wallet/custody API: Manages the keys, signs transactions, handles addresses. Has its own security model and its own transaction lifecycle.

Seven APIs. Seven documentation sets. Seven sets of error codes. Seven authentication models. Seven webhook formats. Seven contract negotiations. And one engineering team trying to make them all behave like a coherent system.

Where the Paradox Bites

Edge case multiplication

Each API handles its own errors. But what happens when the FX API returns a rate, the compliance API flags the transaction, and the payment processor has already initiated the transfer?

The interaction between error states across APIs creates failure modes that no individual vendor tested for, because they don’t know about each other’s systems. Your engineering team discovers these edge cases in production, not in the sandbox.

Reconciliation as a full-time job

Every API generates its own transaction records with its own IDs, timestamps, and status labels. Matching a single payment across seven systems requires a reconciliation layer that is itself a significant engineering project. At scale, this either becomes a dedicated team or a dedicated vendor (which makes it eight APIs).

Version drift

APIs evolve independently. Vendor A ships a breaking change in Q1. Vendor B deprecates an endpoint in Q2. Vendor C changes their webhook format in Q3.

Your integration, which was working fine last year, accumulates maintenance debt as each vendor pursues its own roadmap.

Vendor lock-in at every layer

The more deeply you integrate with seven vendors, the harder it becomes to replace any one of them. Each switch requires rebuilding the integration and re-testing every edge case interaction with the remaining six.

The multi-vendor stack that was supposed to give you flexibility actually reduces it over time.

Why the Industry Got Here

The API-first movement was an improvement over what came before (batch files, proprietary protocols, manual integrations). The problem is that the movement optimized for the wrong unit. It made each component better without making the system better.

This happened because each vendor is incentivized to build the best version of their layer, not to reduce the number of layers. An FX provider doesn’t benefit from consolidating with a compliance vendor. A settlement network doesn’t benefit from incorporating on-ramps. The fragmentation isn’t a design flaw. It’s a business model.

The One-API Alternative

The alternative isn’t going back to monolithic systems. A few infrastructure providers are already moving toward consolidation. The architectural question is where they draw the boundary. Most stop at a layer: on-ramp plus off-ramp, or custody plus transfer.

The more useful design boundary is the full payment journey.

When on-ramp, settlement, off-ramp, and wallet infrastructure are accessible through a single API, the edge case multiplication disappears (one system, one set of error states). Reconciliation simplifies (one transaction ID that spans the full journey). Version drift vanishes (one API to maintain). And vendor negotiation collapses from seven annual cycles to one.

This is the architectural principle behind the Open Money Stack.

Polygon’s network has processed $2.4 trillion in stablecoin transfer volume. The Open Money Stack is being built to expose that infrastructure, plus fiat on-ramps (via Coinme) and wallet infrastructure, through a single integration point.

The goal is, not only, to be the best API. It’s to be the last one you need for the core payment flow.

Simplify Your Payment Integration

Learn more at polygon.technology, or talk to our team about what a single-API payment stack looks like for your cross-border flows.

Custodial vs. Non-Custodial Wallets: Which One Should Your Platform Build?

Move Money Between Solana and Polygon, Ethereum, Base + more EVM Chains with Polygon OMS

.CXtdIGFA_Z2ODqj.webp)

Ithaca Upgrade Is Live: Payments on Polygon Chain Are More Reliable Than Ever

Kansai Electric Power's Rewards Arm Turns Loyalty Points Into Real Stablecoin Payments on Polygon Chain

Mento Protocol Launches on Polygon for Local Currency Stablecoin Payments

PayPal USD Lands on Polygon Chain, Enabling Regulated Onchain Dollars to Move Across Borders in One Integration

Credible Races Past $152M Total Payments Volume on Polygon

We Built the Best Blockchain for Payments. Now We’re Bringing the World’s Enterprises Onchain

Uquid Integrates Polygon's Open Money Stack for 1-Click Crypto Checkout Across 178M+ Products

.Cfn0LZ0R_2iwkGz.webp)