.wqi0pS0q.png)

tl;dr:

- Most enterprise stablecoin discussions focus on USDC and USDT. But non-USD stablecoins (pegged to the euro, Mexican peso, Australian dollar, and other currencies) are growing rapidly and matter for specific corridors.

- Polygon leads all networks in non-USD stablecoin activity, with over $11.1 billion in lifetime volume for local-currency stablecoins, representing more than 43% of all such transfers across chains.

- For enterprise payment teams operating in LATAM, Europe, or APAC corridors, non-USD stablecoins can reduce FX conversion steps and costs by keeping the payment in the destination currency through more of the journey.

- This is an emerging category. Coverage is uneven, liquidity varies by currency, and most enterprises will still use USD stablecoins as the primary rail. But the trajectory matters for corridor-specific payment optimization.

When enterprise teams evaluate stablecoin payments, the conversation almost always centers on USDC and USDT, both pegged to the US dollar. For good reason: USD stablecoins represent over 93% of the total stablecoin market and are the de facto standard for cross-border settlement.

But there’s a growing category of stablecoins pegged to other currencies that matters for specific enterprise payment corridors. And Polygon is where most of this activity is happening.

What are non-USD stablecoins?

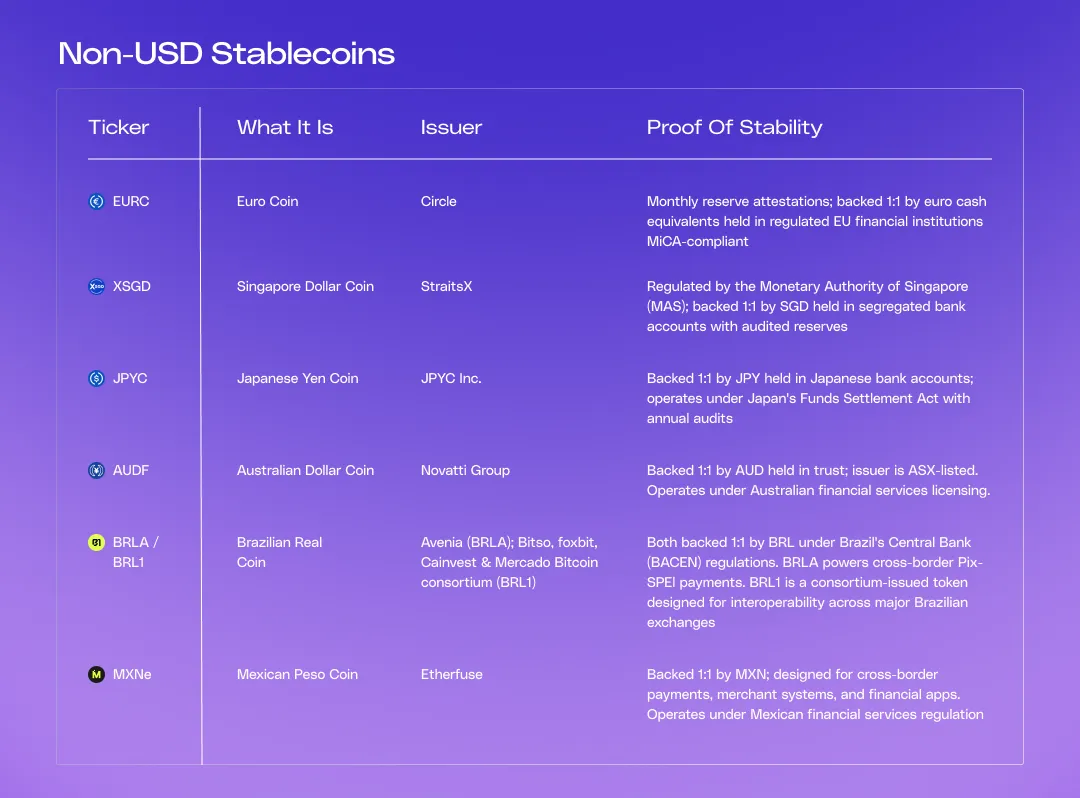

Non-USD stablecoins are digital tokens pegged 1:1 to a national currency other than the US dollar. Examples include EURC (euro, issued by Circle), MXNe and similar Mexican peso stablecoins, AUDD and similar Australian dollar stablecoins, and a growing range of others covering the Brazilian real, British pound, and Singapore dollar.

They work the same way as USDC: issued by a regulated entity, backed by reserves in the pegged currency, redeemable at par. The difference is that they allow payments to stay in the destination currency through more of the settlement journey, potentially reducing FX conversion steps.

Why this matters for enterprise payment flows

In a standard stablecoin sandwich using USD stablecoins, a payment from the US to Mexico involves two FX conversions: USD to USDC (at the on-ramp), and USDC to MXN (at the off-ramp). The cost and speed of that second conversion depend on the off-ramp provider’s MXN liquidity.

With a Mexican peso stablecoin, the flow changes. The payment can convert directly from USD to a peso-denominated stablecoin at the on-ramp, transfer across the settlement network, and arrive in the recipient’s local currency representation with one fewer conversion step. Or, in a peso-to-peso corridor (like a remittance from a Mexican worker in one country to a family member in Mexico), the payment can stay in pesos the entire way.

The practical benefit depends on corridor-specific liquidity, the availability of reliable non-USD stablecoin issuers, and the maturity of on-ramp and off-ramp infrastructure for that currency. In some corridors, this is already working. In others, it’s still early.

Polygon’s position in non-USD stablecoins

Polygon processes more non-USD stablecoin activity than any other network. The numbers: over $11.1 billion in lifetime volume for local-currency stablecoins, representing more than 43% of all non-USD stablecoin transfers across all chains.

This includes Mexican peso stablecoins in remittance corridors, Australian dollar-backed stablecoins, and euro-denominated stablecoins. In one recent week, international (non-USD) stablecoin movement across all chains totaled $195 million, with Australian dollar-backed stablecoins leading that particular period.

The activity is concentrated in corridors where FX costs are highest and correspondent banking access is most constrained, exactly the corridors where stablecoin settlement provides the most value.

What’s ready today and what’s still developing

Ready now: EUR

EURC (euro) has significant liquidity and is issued by Circle, the same regulated issuer behind USDC. Enterprise teams operating in European corridors can use EURC today with established on-ramp and off-ramp infrastructure.

Moving fast: MXN and AUD

Mexican peso and Australian dollar stablecoins are seeing rapid volume growth on Polygon but the issuer and ramp infrastructure is still maturing. Enterprise teams should evaluate counterparty risk and liquidity carefully.

Watch list: BRL, GBP, SGD

Stablecoins pegged to other currencies (BRL, GBP, SGD) exist but liquidity and infrastructure coverage vary significantly. These are worth watching for corridor-specific optimization but may not be enterprise-ready in all cases.

For most enterprise payment operations today, USD stablecoins remain the primary rail, with FX conversion happening at the off-ramp. Non-USD stablecoins are a corridor-specific optimization that will become more important as liquidity deepens and issuer infrastructure matures.

What changes in the next 12 months

Three developments that will accelerate non-USD stablecoin adoption for enterprise payments:

- Regulated issuers expanding coverage. Circle’s EURC is the template — a regulated, transparent issuer extending USDC-grade infrastructure into a second currency. Every additional issuer that follows that model moves enterprise confidence forward.

- The GENIUS Act’s foreign issuer path. The Act provides a route for stablecoin issuers from comparable jurisdictions to operate in the US. Licensed local-currency stablecoins entering the US market would accelerate enterprise adoption of multi-currency stablecoin programs on a compliance footing that treasury and legal teams can defend.

- Ramp infrastructure depth. Stablecoins are only useful at the edges, where they convert to and from fiat. As licensed ramp providers expand coverage in each currency, local-currency stablecoins become progressively more deployable for enterprise treasury.

Explore corridor-specific payment infrastructure

For most enterprise payment programs today, USD stablecoins will remain the primary rail. Non-USD stablecoins are a corridor-specific optimization — already working where liquidity is deep, worth piloting where it’s growing.

Polygon Open Money Stack is being built for both. A single stack that gives banks, fintechs, and enterprise treasuries access to USD and non-USD stablecoin rails across every corridor where the volume is happening — with the same settlement infrastructure, the same compliance surface, and the same single counterparty on Polygon’s side.

If you’re evaluating where your stablecoin program should run, the corridor data is already pointing at one answer.

Talk to the Polygon OMS team →

Custodial vs. Non-Custodial Wallets: Which One Should Your Platform Build?

Move Money Between Solana and Polygon, Ethereum, Base + more EVM Chains with Polygon OMS

.CXtdIGFA_Z2ODqj.webp)

Ithaca Upgrade Is Live: Payments on Polygon Chain Are More Reliable Than Ever

Kansai Electric Power's Rewards Arm Turns Loyalty Points Into Real Stablecoin Payments on Polygon Chain

Mento Protocol Launches on Polygon for Local Currency Stablecoin Payments

PayPal USD Lands on Polygon Chain, Enabling Regulated Onchain Dollars to Move Across Borders in One Integration

Credible Races Past $152M Total Payments Volume on Polygon

We Built the Best Blockchain for Payments. Now We’re Bringing the World’s Enterprises Onchain

Uquid Integrates Polygon's Open Money Stack for 1-Click Crypto Checkout Across 178M+ Products

.Cfn0LZ0R_2iwkGz.webp)